Is AI Really a Bubble ?

Major predictors of the 2008 subprime crisis are questioning the investments being made by big firms and VCs into the AI pool. Raghuram Rajan (former RBI governor of India), Howard Marks, and Michael Burry-big names who actually spotted or identified the bubble-are now worried on multiple fronts. Let’s just break down and connect the dots on whether the bubble will burst or not.

Before starting the macroeconomic and market analysis over whether AI is a bubble, let’s just go through the present scenario of what is actually happening in the global and domestic markets. The FED recently announced a 25 bps interest rate cut due to rising concerns over unemployment rather than inflation. Powell was seen as more concerned about the unemployment situation than inflation, as he sees more downside risk. On the domestic front, we had a 25 bps cut by the MPC due to benign inflation, which opens room for further growth in the economy. In Q2, India recorded growth of 8.2 percent, which is a very good number outlay. But what needs to be questioned is: did we need a cut at all?

For the majority of this blog/article, I will stick to the US economy because the biggest investment laid in AI is done by the US.

As a student of finance, I keep a detailed track of what economists like Raghuram Rajan or investors like Howard Marks say about the economy and the market in general. As this AI bubble is becoming a hot topic, let’s just break down and analyze what their opinions are and analyze them further.

MACROECONOMIC ANALYSIS

As the FED recently announced a rate cut, major economists and investors are asking whether this cut was actually needed. After such a long government shutdown, did the FED have enough data to conclude that the rate cut was needed, or was this due to TRUMP pressure? As monetary easing brings “excess credit” into the market, the US tariff effect is yet to be seen on growth and inflation. By cutting interest rates, they pushed a massive credit expansion, and too much credit is bad for the economy.

But Why ?

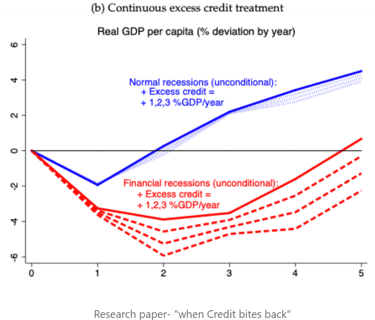

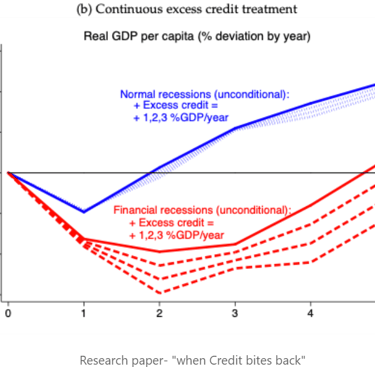

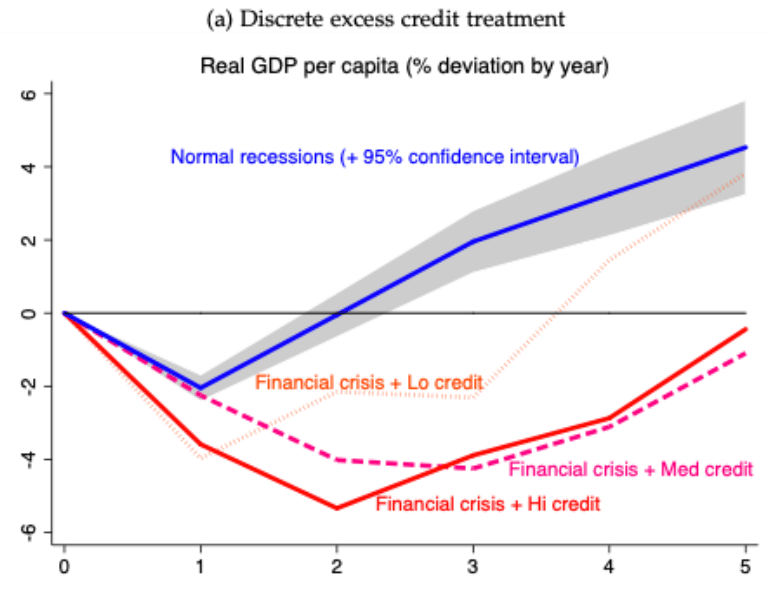

I studied a research report named “When Credit Bites Back: Jordà, Schularick, and Taylor (2013)” where they examine the effects of excess credit. When they examined 154 business cycles in 14 advanced economies, their findings stated that financial crisis recessions- which are worse than normal recessions—are closely related to the credit intensity of expansion.

As we can see, the dip is mainly due to easing in monetary policy starting to bottom out. When monetary tightening starts to take place, there is an excess liquidity requirement in the economy which is not fulfilled, resulting in a recession.

Why do low rates precipitate risk-taking?

Because then households start chasing higher yields, which further increases their risk appetite due to FOMO. So, people start to imitate the investment ways of others if they are being successful. This term is defined as “herding” in economics. So, they start putting money into riskier assets without even analyzing.

We talked about the monetary policy effect. Let’s understand another instrument, which is liquidity expansion and contraction. The expansion of liquidity (increasing the size of the balance sheet of the central bank) is termed quantitative easing, whereas contraction is termed quantitative tightening.

As liquidity expansion increases reserves-which are liquid assets but low-yielding assets for banks—they tend to lend in the short term. This further becomes excessive, resulting in “CREDIT EXPANSION.”

Now, liquidity is like a drug; the more you use it, the more you want it.

WHY WORRY?

Because there is plenty of liquidity in the market, which results in asset prices going up subsequently. Now it is much harder for Central Banks to pull back. The FED started expanding their balance sheet post-2008 crisis, which has now risen to 6-7 trillion from 807 billion dollars because the system now requires more and more liquidity.

Banks provide liquidity to private credit suppliers to participate in the credit cycle without carrying risk on their own balance sheets.

How does the bank carry it without taking risk?

Because banks don’t deploy capital upfront; they extend committed lines of credit—essentially a promise to provide liquidity when required. These facilities are senior and backed by high-quality collateral, ensuring that most of the credit risk remains off the banks’ balance sheets.

HOW is this an impact on the AI bubble?

As these private lenders are heavily optimistic about the AI ecosystem without even knowing the future outcome or how they will be able to generate cash flows, these lines of credit go into these riskier investments. This remains masked due to excess liquidity. But once monetary policy is tightened, liquidity shrinks, which raises the probability of overstretched valuations, and hence the correction unwinds sharply.

We are still in the EARLY DAYS.

MARKET’S PERSPECTIVE - (Burry and Mark commentary)

We’re going to see what Michael Burry, renowned for predicting the 2008 subprime crisis, has to say about the AI bubble and do a deep dive analysis on whether these claims are worth seeing or not.

"BIG SHORT" Investor Michel Burry accuses ai Hyperscalers of Artificially Boosting Earnings

He warns that the big AI companies (MAGA 7) are tweaking the estimated useful life to show inflated operating income. These are under the rights of management to change the estimates, but what is concerning is that for decades the industry standard was 3 years. Post the cloud era, AWS and Azure claimed to have developed sophisticated software which can still extract data from old servers, which made them increase the estimated asset life from 3 years to 4 or 5 years.

BUT WHAT HAPPENS WHEN THE ESTIMATED ASSET LIFE IS EXTENDED?

When the EUL (Estimated Useful Life) of a company is extended, the depreciation charged is divided as per the matching principle. So, the depreciation amount gets lower, which further inflates the operating income of the company. And it distorts the valuation as the P/E ratio looks reasonable, making the stock look cheap.

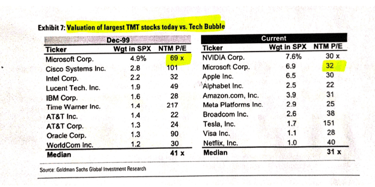

CONNECTING THE DOTS-(2000 DOT COM BUBBLE)

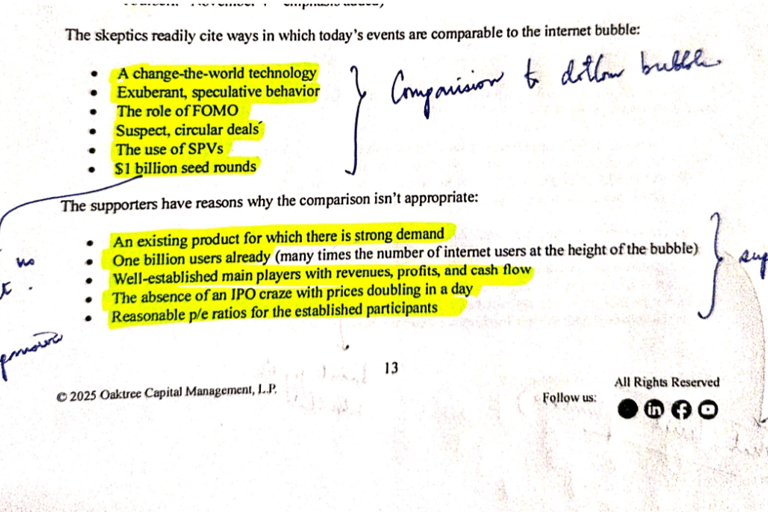

You have likely heard many investors and influential people discussing the similarities between the Dot-com bubble and the AI optimism currently flowing through the market.

Let’s decode these claims to understand whether they are worth our concern or not.

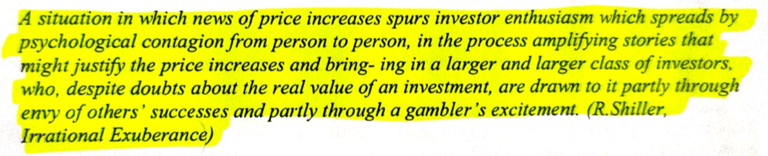

I am attaching a snapshot from a recent Howard Marks memo, dated December 4, 2025, where he speaks a little about this similarity. However, there are two bullet points in the supporting framework that I don’t entirely agree with. Let’s discuss and understand why.

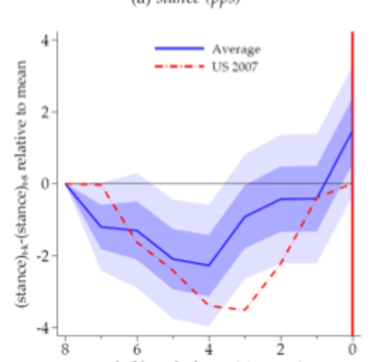

As we can clearly see, when credit expansion is high, the intensity of the recession also worsens.

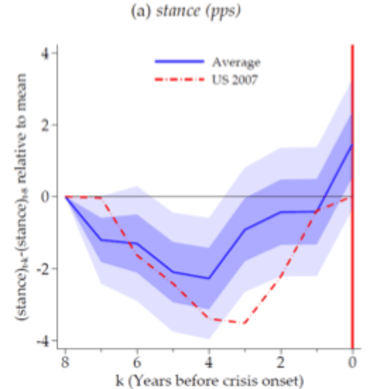

How is it even related to monetary policy?

Because the policy stance and credit growth before the crisis are really important for us to analyze. For this, we will see the policy condition just before the 2008 financial crisis.

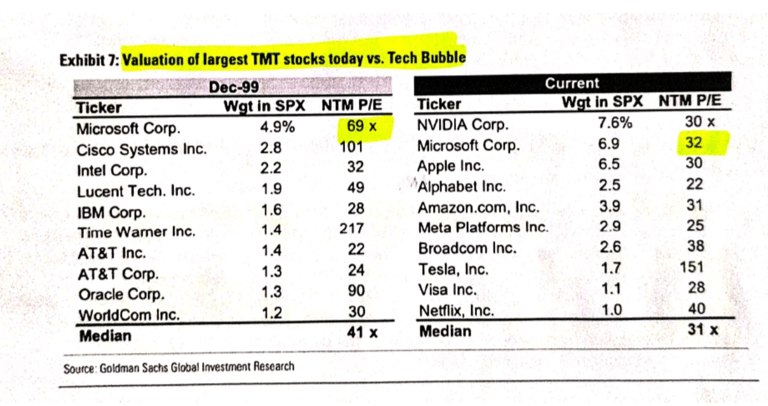

Supporters argue that the P/E ratios for established firms are reasonable. But I don’t buy that claim. Why?

The Adjusted P/E Model To understand true valuation, one must adjust earnings to reflect "realistic" depreciation changes.

Hypothetical Adjusted P/E Calculation:

Reported Net Income: $62 Billion

Depreciation (due to EUL change from 5.5 years to 3 years): Estimated to be around $10–12 Billion annually

Adjusted Net Income: $50 Billion

Current Market Cap: $1.6 Trillion (Hypothetical)

Reported P/E Ratio: 25.8x

Adjusted P/E Ratio: 32.0x

The stock becomes significantly more expensive than it appears. A 32x multiple implies hyper-growth, and if AI earnings slow, there could be multiple contraction.

I totally understand that these numbers are not as extreme as Dot-com bubble P/Es, but momentum starts to build when there is too much euphoria in the market.

Howard Marks very rightly said that whenever there is too much optimism in the market, people tend to forget the real value of a company and its future earnings. He quotes Warren Buffett saying